Since they emerged in the 80s and 90s, structured products have provided an effective source of funding for investment banks and companies as well as attractive tailored investments for asset managers, financial advisers, and retail investors.

With new regulatory requirements under Packaged Retail Investment and Insurance Products (PRIIPs) soon coming into force, and in a post-pandemic world where economies are struggling with rising costs and dropping standards of living, what value do structured products offer to both those writing them and those investing in them?

Read on for a breakdown of all things structured products, or use these links to jump to the info you need.

TTMzero: Automated solutions for capital markets

One of United Fintech's portfolio companies, TTMzero, provides high-quality real-time data and fully digitized regulatory and capital markets tech solutions that take clients into a new digital era.

To learn more about TTMzero's solutions, click on the products below:

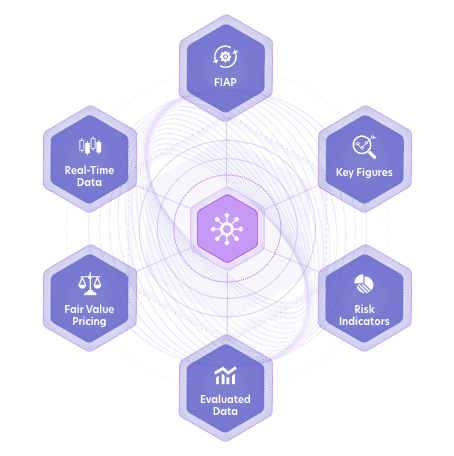

Products

Key Figures and Risk Indicators

TTMzero calculates about 100 key figures for structured products, including the Greeks and risk indicators, which provide precise risk and return probabilities.

Financial Instruments Automation Platform

Digitize your issuance processes with TTMzero’s Financial Instruments Automation Platform (FIAP) to allow for a fast market launch of new products and ensure straight-through workflows. Also includes PRIIPs for KIDs.